Following the proposal made in the Union Budget 2025 by the Finance Minister for expanding the scope of safe harbour rules, the Central Board of Direct Taxes (CBDT) has introduced certain amendments vide its notification No. 21 dated 25th March 2025. These amendments are aimed at reducing litigation and providing certainty in international taxation. Let us explore the amendments and their corresponding impact on the business in this edition of our TaxWire.

Background

Safe harbour rules are simplified compliance guidelines for resident Indian entities dealing with their foreign group entities. Instead of going through detailed documentation and scrutiny to prove fairness in international transactions, eligible businesses and transactions can follow a pre-defined path prescribed in the Income Tax Regulations, where they get acceptance of pricing to be at arm’s length without further questioning.

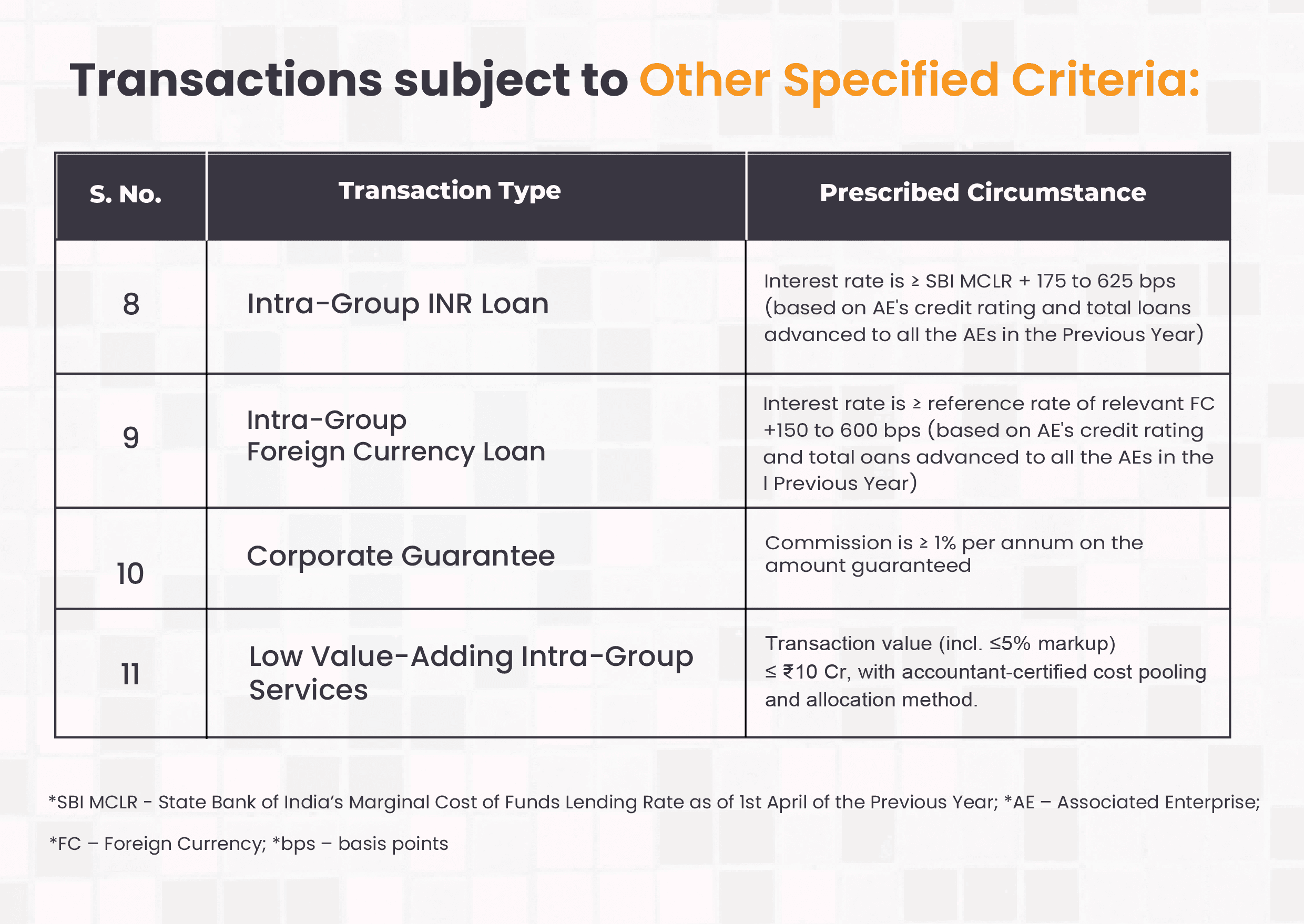

These rules foster simplification of compliance, reduce litigations and disputes, and offer certainty for eligible international transactions in the area of software development services, IT-enabled services, intra-group loans, corporate guarantees, manufacture and export of auto components, etc.